Check out 5 impressive benefits of Gigantiq By ETIQA!

Gigantiq by ETIQA

GIGANTIQ is not a bank account or a fixed deposit. It is a single premium, yearly renewable, non-participating universal life plan denominated in Singapore dollars

Why Gigantiq?

High interest rate: 1% PA guaranteed and 1% bonus for first year (on your first $10,000)

Convenient : Manage your account anywhere on an app

Flexible: No lock in period

Life protection: Death coverage of more than 100 percent of your account value

Capital guaranteed: get back your full capital whenever you need the fund

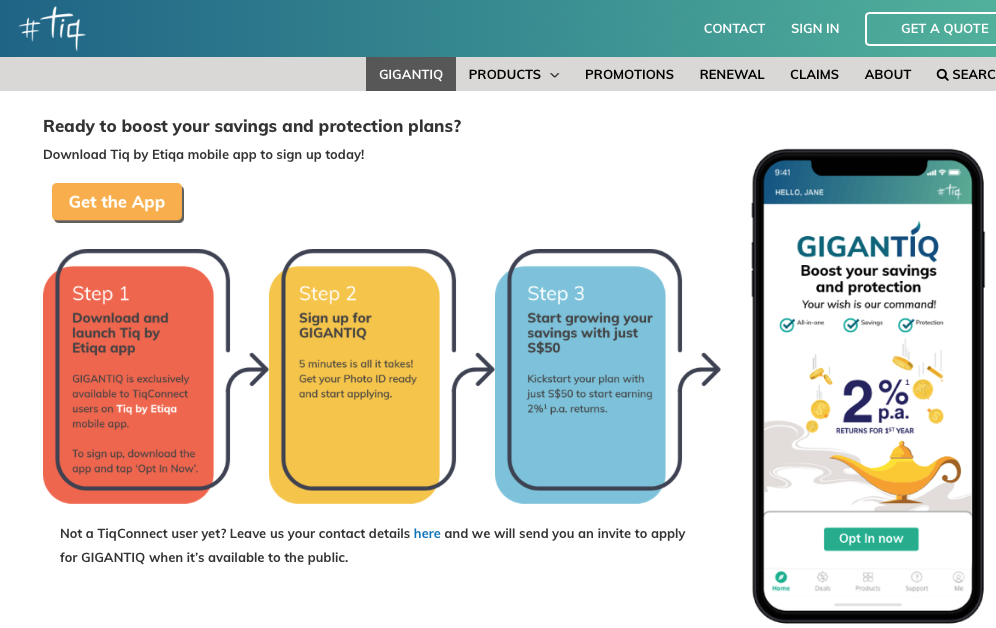

How to apply Gigantiq?

Firstly, download their application, Tiq by Etiqa on your mobile!

Then get ready your photo ID and set aside 5 min to register for Gigantiq.

Finally, top it up with just $50 to get your money rolling!

Gigantiq VS Elastiq

Both are universal life plans.

The greatest difference is the guaranteed interest rate. Elastiq guarantees 1.80% p.a. for the first 3 years, however 2.00% p.a. under Gigantiq is only guaranteed for the first year.

Minimum amount in Elastiq is $5,000 else you may face additional charges, while Gigantiq only requires average daily Account value for the calendar month to be above S$50.

More benefits for Elastiq: A non-guaranteed bonus of 0.3% of the average monthly Account value for the past 36 Policy months will be given every 3 years, if no withdrawal has been made before.

Gigantic VS Dash Easyearn Vs Singlife

Heres's a quick summary:

The Gigantiq account indeed works as an idea for guaranteed interest that has NO lock in period.

All these accounts are better than the Singapore Savings Bond in my opinion.

In addition, for anyone seeing this comparison for the first time, Singlife’s account may look more attractive at 2.5% and it should be the first account to fill.

But personally, I will choose not to put too much of my money in such accounts. I would be more inclined to diversify my funds in other areas of investment.

Gigantic VS SCB Jumpstart account (For age 18-26)

Jumpstart is a savings account for young adults age between 18-26.

The interest rate is 1% for up to $20,000. It even comes with a debit card with up to 1% cash back.

With no lock in and no minimum spend.

Personally, I would choose to stay with Jumpstart. This is mainly credited to the fact that jumpstart has its first movers advantage.

As a student this is meant to be my savings of my allowances which do not come in great amounts. Having to transfer my existing balance and create a new account would be a hassle.

Additionally, as someone who dislikes holding cash, most if not all of my payments are made digitally. Hence, the debit card with 1% cash back is the most attractive point from my point of view.

Final words

Insurance companies today are starting to leverage on technology to compete for idling banking depositors' monies idling.

There is a shift of traditional fixed term endowments plans into a more flexible, app-based, trendy plan that can appeal to forumers and we should see more such plans from other insurers soon.

Insurers will likely upsell protection plans by giving higher interest. Similar to how banks have been doing with all the OCBC360 and DBS Multiplier. This is shown in the “coming soon” feature for GIGANTIQ.

PS: Video for you on How You can DOUBLE your money!

Leave a Reply